With the rising cost of utility bills, more and more clients are asking us about what they can claim for working from home given, for many, this is the new norm.

HMRC state that an employee, director or the self-employed may claim for their use of room as office as long as it is “reasonable”. The question however is “what is reasonable?”

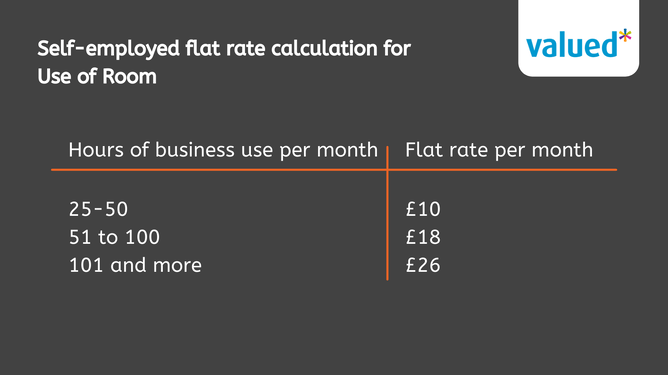

1. The flat rate – Available to the Self employed only

HMRC have devised a simplified claim for use of room based on the number of hours worked from home in a month. The categories are as follows:

The rates were originally created for the self-employed but with the recent rise in people working from home during the pandemic, the use of room was available to all staff members. However, since our return to offices, HMRC states that if there is the availability to work from an office then no claim can be made.

2. The actual cost basis (normally providing a greater claim) - Everyone

The more common approach for those that can reasonably prove that they have a dedicated office space is to claim for the actual cost. For this to be proven HMRC would require supporting documentation in the form of utility bills and a prepared calculation. This has become easier with the support of smart meters but can be challenged by HMRC at any stage.

Items which can be claimed include:- Gas, Electric, power costs

- Home telephone calls

- Insurance – if covering the business equipment

- Broadband (the contract should have started after the period of working from home)

- Invoiced cleaning costs

- Repairs and maintenance on business items

- Rent or mortgage interest or mortgage capital as these would have been paid for anyway. Unless the rent is wholly and exclusively for business purposes i.e. the rent of an office space or storage unit.

- This however is different for a sole trader; a proportion claim could be made for rent or mortgage interest.

Calculating the claim:

After adding up all the total costs above, the claim can then be calculated using one of the following methods:

% Space Method

Calculate the proportion of household space used for business against the number of usable rooms (excluding the kitchen and bathroom). Alternatively, you can claim on the square meterage of the rooms.

Time Method

Calculate the claim on the time the space is used for business e.g., hours per week used for business divided by total hours. More common in small bedsits or apartments where occasionally there is only one usable room.

% Space Method x % Time

For areas of the home used for dual purpose e.g., the dining room, a claim of % space x % time could be used to give a more accurate representation.

It is important when making a regular claim to discuss this with your accountant, as it may have implications on capital gains tax upon sale of your home or business. If you do not have an accountant, please get in touch and we will be happy to help.

The claim will be paid as a business expense on a monthly or annual basis for employees or directors. The use of Xero expenses can help with this. Alternatively for directors your accountant can offset this against your director’s loan or for sole traders, include it as a tax deductible expense in your accounts.